Русский

Русский

English

English 官话

官话 português

português عربي

عربي Türk

Türk

.jpg)

Does the UAE real estate market need new financing rules?

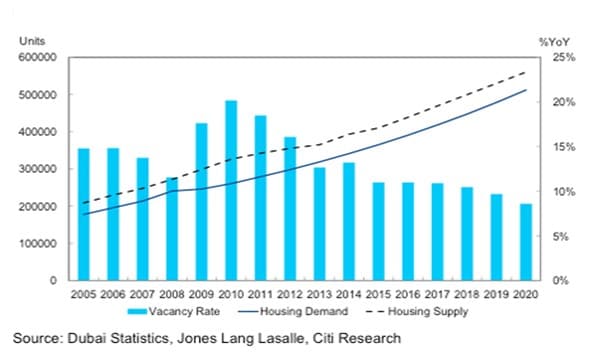

The United Arab Emirates (UAE) property market has experienced quite a few major developments within the past decade, with a host of new laws, initiatives, and real estate projects being announced. Moving into 2019, the UAE real estate market has been characterised with a great deal of positivity and improvements. Over the past five (5) years, the UAE real estate sector has been in a continuous remedial phase. For instance, the UAE’s property market peaked in mid-2014.

According to rating agency Standard & Poor’s (S&P), the UAE property market, particularly in the Emirate of Dubai, will witness encouraged and enhanced recovery beyond 2021. Hitherto, investors have maintained a wait-and-watch stance on the property market, in spite of positive initiatives being taken up by real estate developers and the governments of the various Emirates. Amid a reasonably positive outlook, property prices have continued to fluctuate, but at a positive stance, since 2014, leading to the creation of buyer’s, market within the past five (5) years.

With the Expo 2020 coming up, which is set to align well with the proposed stabilisation of the UAE property market, there is an uptick in the market related to the Expo. The Expo 2020 has already been taken into account into the property market, and the impact of the same had already been absorbed, thus perhaps accounting for the peaking of property prices in the Emirate of Dubai in mid-2014, given the Expo’s announcement in late 2013.

UAE Government Policies & Industry Response

The UAE government has initiated a host of new changes to the real estate sector, to strengthen the industry and its fundamentals prior to embarking on the journey towards rejuvenation in the following couple of years.

Perhaps one of the most publicised of such initiatives has been the institution of a 10-year residency visa for long-term foreign investors, along with a 5-year retiree visa, in 2019. Requirements for qualifying for the 10-year visa include, inter alia, public investments by an individual amounting to at least AED 10 million, and requirements for the 5-year visa necessitate the investing of AED 5 million into a property by the individual. Such initiatives have been instituted with the hopes of reinvigorating interest the UAE property market and increasing demand for real estate in the midst of the current oversupply of properties that exists in the UAE.

In the Emirate of Abu Dhabi, property ownership laws were amended to permit freehold ownership by foreign investors for the first time in particular economic free zones. All across the Emirates, authorities have sought to further reduce government fees required to pay for property registration and real estate transactions, further relaxing the restrictions on foreign ownership in the efforts to create a more conducive environment for property investments.

The Dubai Land Department (DLD) even launched a real estate self-transaction (REST) to facilitate quicker and more efficient means of processing real estate transactions. The REST platform has allowed for the digital management of all property transactions from 2018 onwards, and REST was launched as a part of the “Dubai 10x Initiative”, a marketing campaign launched by the Dubai government to market Dubai as “the most innovative city on Earth in 10 years”. The Dubai Real Estate Regulatory Authority (RERA) also launched a smartphone application named “Taqyimee”, that offers real-time market prices for properties, and connects real estate owners to investors, thereby reducing factors such as time and cost involved in the sale of real estate. The DLD hopes that the institution of such digital platforms would increase transparency in the Dubai property market, thereby making it more investor-friendly and providing a greater degree of access to the market to property buyers.

In Dubai, a great deal of property developers such as, but not limited to, have sought to “simulate” demand through employing various creative strategies. Such strategies have included rent-to-own schemes, allowing post-handover payments, sale-and-leaseback models, ensuring investors cannot resell until completion of set time or certain percentage of payments, and acquiring bank finance for the initial down payments of properties. Some of these aforementioned offerings pave way for rental revenues and returns for investors on behalf of the property developer, or 10-year payment plans for financing homes, that allow for payments to be made years after completion of real estate projects. Such initiatives have seen varying levels of success across the Emirates, but continue to have a profound effect on the UAE’s real estate market. A recent Bloomberg Business survey revealed that Dubai was at the least risk of a property bubble (compared to Munich, Toronto and Hong Kong that were set at top of the list).

Perhaps the more extensive solution to this issue lies in the resolution of credit issues in the region with regards to real estate and analysing the mortgage laws that govern the sale of properties in the UAE.

UAE Mortgage Laws & Financial Developments

Financing a property is the key question that constitutes an individual’s decision whilst purchasing a property. Most investors in the UAE property market take a mortgage to finance their purchase. For simplicity purposes, this article shall further only concern the Emirate of Dubai.

Dubai’s mortgage law pertains to Law Number (9) of 2009, which amended certain provisions of Law Number (13) of 2008, which regulated the interim real estate register in Dubai, and was otherwise known as Dubai’s “Mortgage Law”. The core elements of the statute are as follows:

- Articles 3 – 6: Articles 3, 4, 5, and 6 define important terms such as a mortgage, mortgagee, and mortgagor.

- Article 7: This article concerns the registration of a mortgage. It states that a mortgage is rendered invalid unless and until it is registered with the DLD, and that any agreement thus formed contrary to this is void. Also, it states that the mortgagor, i.e., the owner of the property shall be the sole bearer of the costs outlined within the mortgage agreement/contract unless agreed otherwise. It stipulates the cost of the registration of the mortgage, which is a fee of 0.25% of the amount of the loan, in addition to AED 4,100.

- Articles 10 – 20: These articles lay out the rights and restrictions of the mortgagee and the mortgagor during the duration of the mortgage.

- Articles 25 – 30: These articles pertain to the relevant execution proceedings that take place on the mortgaged property. This outlines the instructions on the manner in which a mortgagee may choose to commence legal proceedings against a mortgagor in the event that the mortgagor is defaulting on his/her payments. This law stipulates that after all the requisite procedures and notice periods are met following the legal proceedings, the property be sold at a public auction.

It is also important to note that this law outlines all the particulars (as specified by RERA) that ought to be accompanied with the mortgage application during the registration process.

However, one of the most contentious issues surrounding the UAE real estate market is the mortgage cap that exists on loans, often described as the “loan-to-value” (LTV) limit on a mortgage. At the end of October 2013, the UAE Central Bank put into effect a new set of regulations on mortgage lending by banks and financial institutions, which entailed finance companies, banks, and other financial institutions to provide mortgages in accordance with “best practices”, so as to better protect borrowers. The Central Bank also issued a threshold of 50% on the amount of an individual’s income that can be committed towards paying off debts, including a mortgage. The figure below outlines the LTV ratios set by the aforementioned change:

| UAE NAtionals | ||

A few key takeaways from the impact of the mortgage cap; thus instituted are as follows:

- For expatriates, mortgages became capped at 75% of the valuation of the first purchase of their property, and similarly, at 80% for UAE nationals.

- Loans exceeding AED 5 million were further capped at 65% of the value of the property for expatriates.

- For villas in Dubai valued from AED 5 million to AED 10 million, an up-front payment (in cash) would be needed to be made of almost 50% of the value of the property. For other property types, UAE nationals and expatriates would be required to make a down payment ranging from 20%-50% depending upon the value of the property.

Many property stakeholders have continuously sought to change the LTV framework currently in place, to facilitate borrowing. Investors reckon that amendments to LTV limits would be able to guide the market towards a more balanced outlook. Investors have also sought to push the UAE Central Bank towards easing age restrictions for mortgage eligibility age limits from the current limits of 65 years for expatriates, and 70 years for UAE nationals, to limits along the lines of 80 years in the UNITED Kingdom (UK), or that of a no-limit level in the United States of America (USA). Amending the aforementioned limits to be based upon the mortgagor’s ability to repay their obligations would seem as a reasonable measure to boost demand.

In September 2018, a federation comprised of the UAE’s leading banks cited the means of an amendment to the UAE’s mortgage rules in order to enhance the real estate market.

Role of Lawyers

It is of high importance to hire a legal professional to under and to legitimize the ownership of the property. Investing in real estate in UAE is a worthwhile option, and now that Dubai is ever-growing as an international economic hub, there is an endless list of services that the Property lawyers in Dubai can advise their clients on. Evidently, foreign investors face challenges in terms of language (e.g. French speaking Canadian property buyer who does not speak English or Arabic desires to buy a property in Dubai on his own without the help of a lawyer or professional), understanding the commercial terms of sale and purchase, becoming aware of financing and possibility of availing the same, reading the fine print in the sale purchase agreement (the SPA) (which as outlined above, often restricts investors to resell their properties for a length of time), and negotiating the SPA. Likewise, investors also seek guidance on matters involving delayed handover, payment of transfer fees to Dubai Land Department, transfer of property to family members or subsidiary firms (which is set at 0.125% of the sale value/market value of the property), post-handover obligations, role of owners association and rights of property owners, default provisions, and insurance obligations, to name a few. These may also include the following: -

- preparing and drafting of legal documentation;

- title search;

- legal filings;

- facilitating the transfer of properties;

- finalising and closing the construction deals; etc

Change in Title and Property Gifts

Our real estate lawyers have assisted majorly, when it comes to transferring gifts and with regards to the transfers which take place between siblings and if the transfer is possible on the same existing property. It is outlined specifically that the DLD shall not permit to conduct transfer via gifts amongst siblings, since only parent to child and husband to wife relationships gain eligibility. Further, it is not allowed to have multiple gift transfers on the same property to circumvent the earlier rule. That means, it is not permissible to transfer the gift from one sibling to the parent and then transferring the same gift to the other sibling. However, the most prominent exception to this rule is the transfer of gifts between companies and individuals.

In high probability it is certainly possible to transfer a specific portion or entire rights in the property without the obligation of paying the transfer fees to the DLD.

Transfer by way of Gifts

Under the transfer by the method of gifts, the process of “Hiba” (in Arabic for gift) allows the first-degree relatives for transferring a portion or entire property rights by way of grant, donation or gift at the DLD. The procedure flows as under: -

- obtaining the no-objection certificate

- payment of transfer fees

- finalising the transfer of title

Conclusion

In conclusion, a raft of the prior proposed changes ought to be instituted to the financing rules that govern the UAE’s real estate market, in light of the recent developments that project the UAE’s property market into the direction of a buyer’s market in late 2020, or early 2021. To alleviate the risks that come along with this transition, and to expedite the recovery process, the UAE Central Bank must consider relaxing limits on its tightened credit rules, so as to facilitate borrowing and make buying property more attractive to a broader demographic of the UAE’s population. While passive measures such as the implementation of a 10-year visa, and the waiving of auxiliary fees on transactions has helped to serve the purpose to a degree to a far more substantive move which would be a push towards hard changes in the legislation that governs mortgage rules in the UAE.